Currently reading a recent draft of Reinforcement Learning: An Introduction by Sutton and Barto. Really good book!

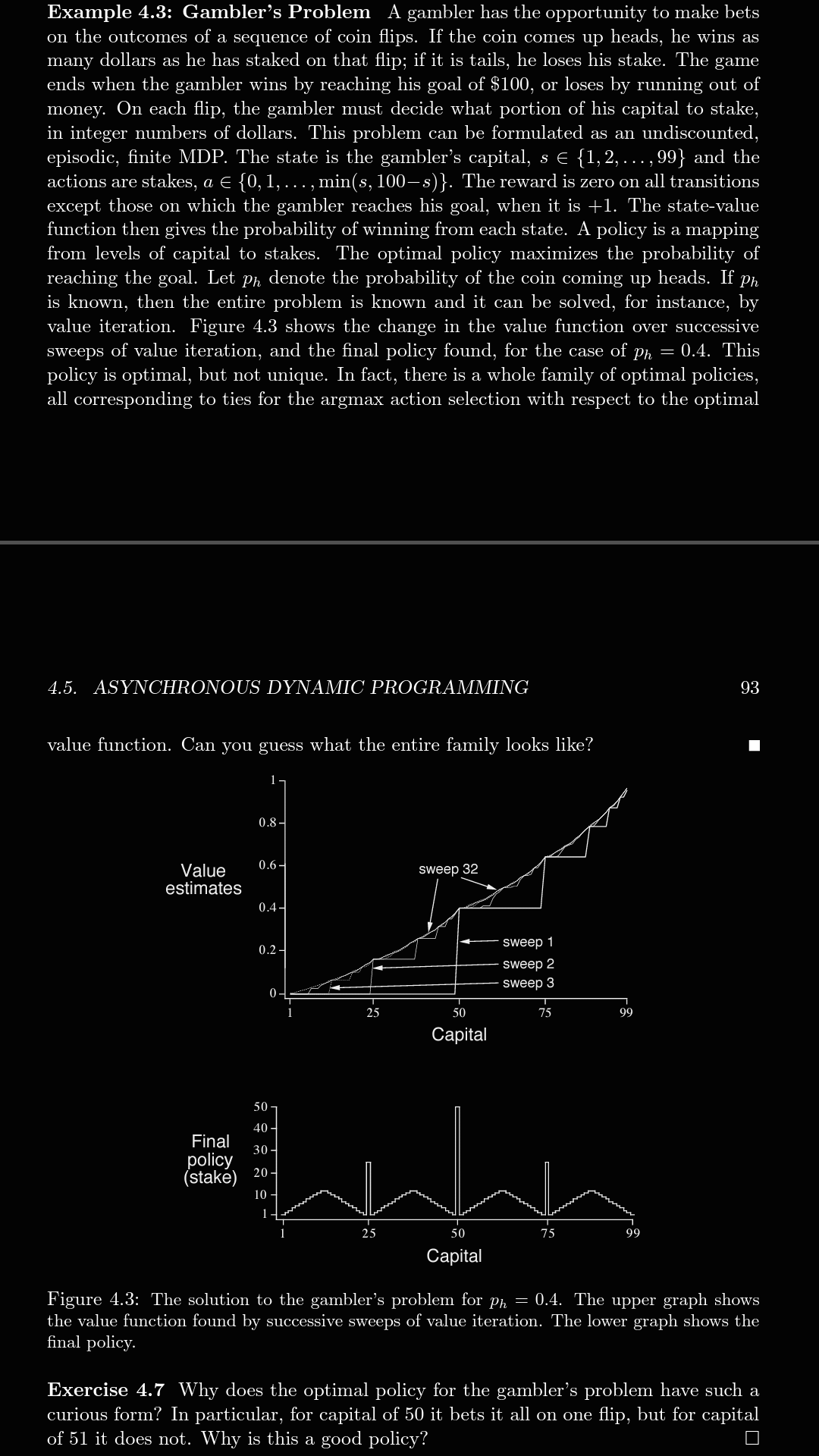

I was a bit confused by exercise 4.7 in chapter 4, section 4, page 93, (see attached photo) where it asks you to intuit about the form of the graph and the policy that converged. I do not understand why this policy is as it is, and was wondering if anyone has any insight into the problem or answers for this exercise in the book.

I have so far look extensively around Google for answer booklets or any work on the problem to no avail. I could not resolve why s=50 would be a bound with a high a=50 when surely any similar policy could be applied to s=51 with a=49? Any help is much appreciated, many thanks!